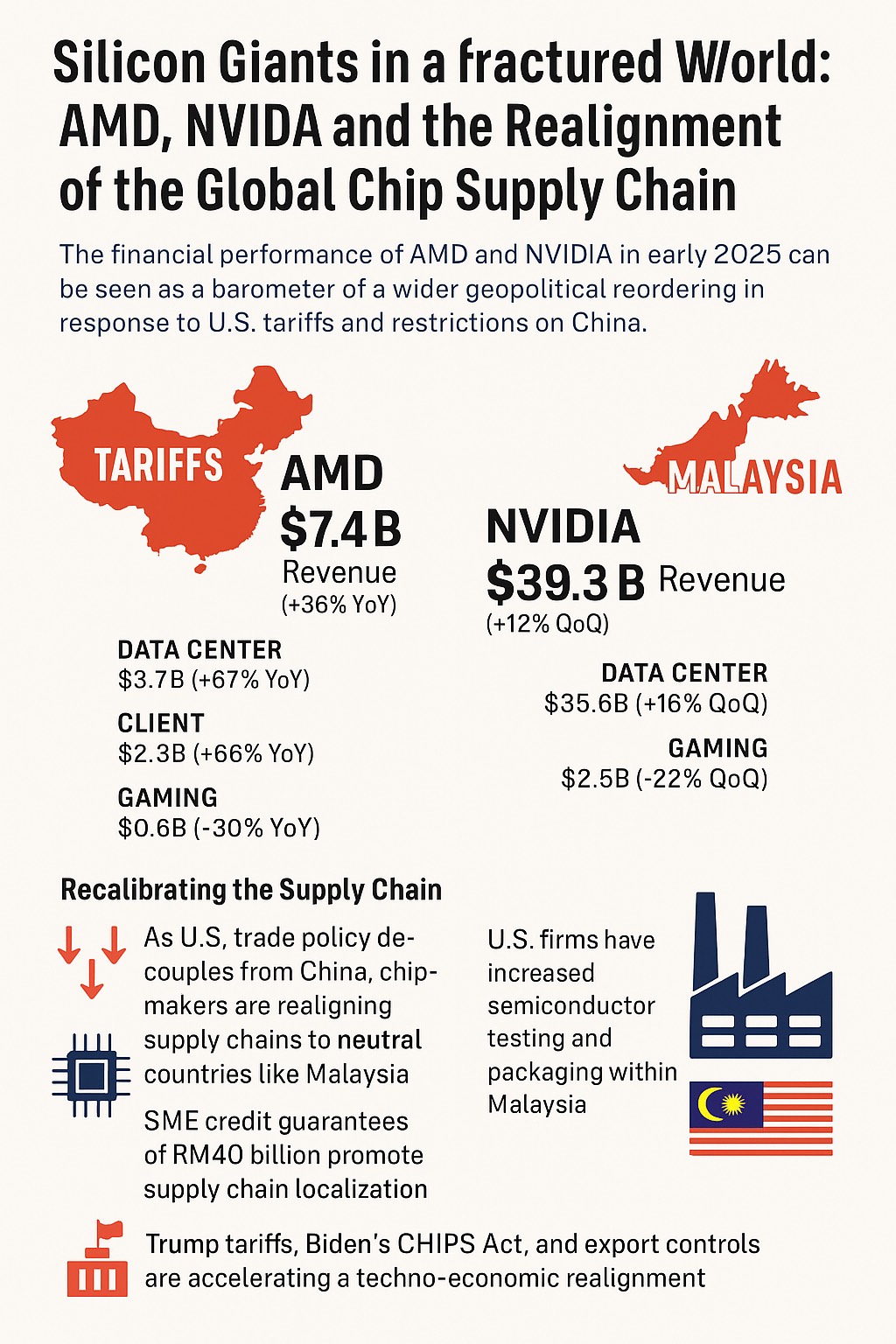

The latest income statements of AMD (Q1 FY25) and NVIDIA (Q4 FY25) are more than just financial snapshots. They’re real-time barometers of a wider geopolitical reordering, one shaped by tariffs, tech wars, and a recalibration of supply chains — in which Malaysia is quietly emerging as a strategic node.

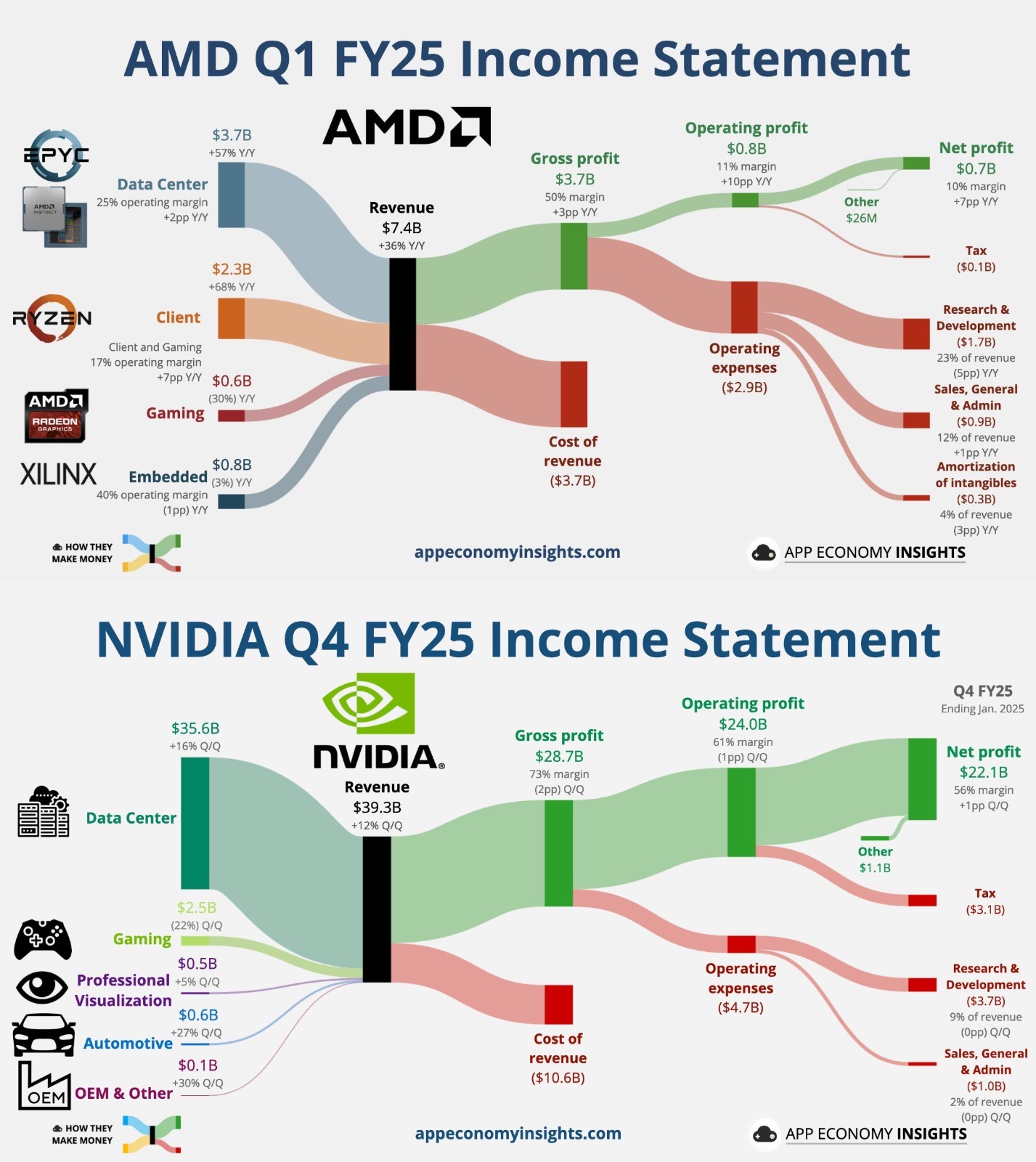

Let’s begin with the raw numbers. AMD posted Q1 FY25 revenues of $7.4 billion, up 36% year-on-year, while NVIDIA, for Q4 FY25, came in with a staggering $39.3 billion in revenue, a 12% quarter-on-quarter increase.

The contrast is stark, not just in scale but in sectoral drivers. For AMD, Data Center revenue rose 57% YoY to $3.7 billion, while Client and Gaming segments pulled in $2.3 billion (+68%) and $0.6 billion (-30%), respectively.

For NVIDIA, Data Center alone delivered a whopping $35.6 billion, up 16% QoQ, with Gaming contributing $2.5 billion, relatively flat.

Yet these numbers don’t just reflect market demand—they map the strategic outcomes of U.S. trade policy. Ever since the Trump administration initiated sweeping tariffs on Chinese imports and targeted Chinese tech giants like Huawei and SMIC with export controls, semiconductor players like AMD and NVIDIA have been forced to reconfigure their upstream and downstream supply chains.

NVIDIA’s outsized Data Center profits — $22.1 billion in net profit with a 56% margin — owe much to AI-driven demand, notably from U.S. hyperscalers like Microsoft, Meta, and Amazon. But more importantly, its success reveals how America’s restrictions on advanced GPU exports to China have created artificial scarcity.

By blocking sales of top-end chips like the A100 and H100 to China, the U.S. has redirected demand inward and toward allied countries. AMD, too, with a more modest net profit of $0.7 billion (10% margin), is adjusting its chip strategy amid similar geopolitical guardrails.

Realignment of the Global Chip Supply Chain

That’s where Malaysia enters the equation. The country has long been a key back-end player in the global semiconductor value chain, especially in assembly, testing, and packaging (ATP).

Post-trade war, it’s evolving into a preferred “friend-shoring” hub for U.S. chipmakers looking to diversify away from China without sacrificing efficiency.

U.S.-based companies have increasingly leaned on Malaysian facilities in Penang and Kulim, many of which are operated by American subcontractors or joint ventures.

The $40 billion credit guarantee push for SMEs announced by Malaysia’s 2025 Budget, for instance, signals a clear intent to scale local participation in the high-tech economy, particularly in electronics manufacturing services (EMS) and chip packaging.

This ties directly to the supply chain recalibration by giants like AMD and NVIDIA, whose chips might be fabricated in Taiwan or South Korea, but are increasingly tested and packaged in Malaysia before global distribution.

Let’s tie this back to costs. NVIDIA’s cost of revenue was $10.6 billion, with operating expenses at $4.7 billion, including $3.7 billion in R&D (9% of revenue) — a figure AMD mirrors proportionally, spending $1.7 billion or 23% of its smaller revenue base.

But the geopolitical price is steeper: NVIDIA and AMD must not only outspend but also outmaneuver regulatory constraints and navigate the tech bifurcation between the U.S. and China. Trump’s tariffs and Biden’s CHIPS Act are two sides of the same coin—strategic decoupling dressed in different fiscal garments.

The recent export controls on advanced AI chips to China, layered with tighter investment screening by CFIUS and Malaysia’s own shift toward national chip policy, signal a new paradigm.

Malaysia, through entities like MIDA and with help from U.S. strategic allies, is now marketing itself not just as a passive manufacturing base but as a neutral node in the techno-political chessboard — attractive to U.S. firms wary of overdependence on Taiwan or facing regulatory cliffs in China.

Even more crucially, Malaysia’s participation in the Johor-Singapore Special Economic Zone (JS-SEZ) and the development of smart logistics, chip clusters, and digital infrastructure form the long game.

With U.S. sanctions reshaping semiconductor demand, Malaysia’s neutral foreign policy and sound infrastructure are making it a default choice in the East’s version of the “Silicon Triangle,” next to Vietnam and India.

So what do AMD and NVIDIA’s financials tell us in 2025? More than just profits and margins, they reveal a techno-economic realignment accelerated by tariffs, tempered by innovation, and quietly enabled by strategic nations like Malaysia.

In a world where AI, chips, and geopolitics increasingly converge, Malaysia isn’t just riding the wave — it’s positioning itself to shape the tide. - DagangNews.com

Samirul Ariff Othman is a geopolitical and economic analyst. He regularly writes on how global macroeconomic trends intersect with trade and industrial policy.

Layari kami terus di DagangNews.com

Orang ramai dipelawa menghantar artikel ke ruangan PARAFRASA di [email protected] mengikut ketetapan berikut:

1. Berbentuk analisis peribadi (Op-Ed) mengenai sesuatu isu atau topik, bukan plagiat

2. Topik yang mendapat perhatian segera dan utama ialah

a. berkaitan perniagaan, perdagangan, keusahawanan, pelaburan

b. Ekonomi MADANI

c. Pembangunan ekonomi negara dan negeri khusus

d. Sektor industri khusus seperti minyak sawit, getah, penerbangan, minyak dan gas

e. ESG

f. Hak pekerja, hak majikan, hak asasi manusia

3. Sains & Teknologi

a. Penemuan penyelidikan Sains & Teknologi serta teori dan konsep

b. Langkah mengkomersialkan produk berasaskan R&D

4. Kaedah penulisan

a) Sebaiknya seorang penulis sahaja pada penama.

b) Berbahasa Malaysia

c) Bahasa Inggeris diterima tetapi akan diterjemah ke Bahasa Malaysia

d) Editor akan memutuskan jika mahu mengekalkan Bahasa Inggeris

e) Tidak melebihi 1,000 patah perkataan dan tidak kurang daripada 600.

f) Jika disertakan gambar, juga amat digalakkan tetapi jangan guna Google (elak langgar hakcipta)

5. Hantar HANYA kepada DagangNews.com

a) Jika didapati artikel sama disiarkan di media lain kerana penulis menghantar merata-rata, nama penulis akan disenaraihitamkan.

b) Sila kemukakan Nama sebenar, Cadangan nama siaran dan emel untuk dihubungi (untuk rekod).