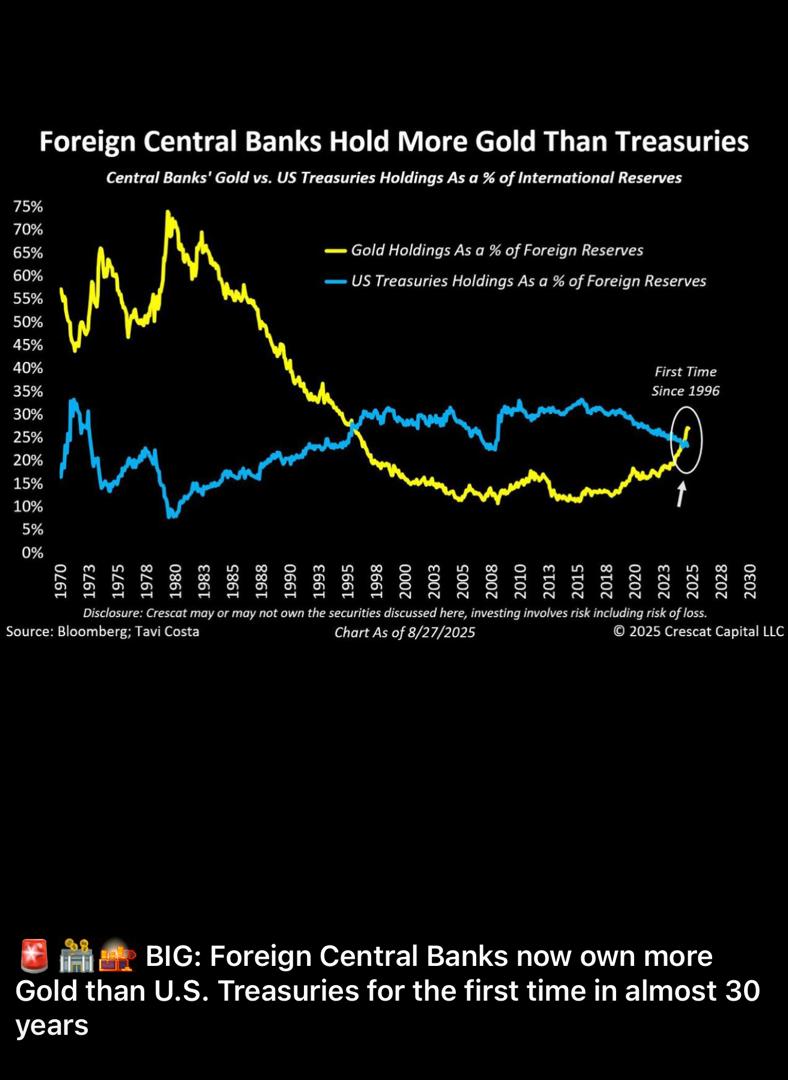

A Turning Point in Global Reserve Management

For the first time since 1996, foreign central banks now hold a larger share of their international reserves in gold than in U.S. Treasuries.

This crossover, as of August 27, 2025, is not a statistical quirk—it is a profound signal of shifting global trust.

The chart, published by Crescat Capital using Bloomberg data, traces over five decades of reserve composition: in the 1970s and 1980s, gold dominated; in the 1990s through the early 2000s, U.S. Treasuries surged in importance.

But now, nearly 30 years later, gold has regained the lead. This moment reflects more than a change in portfolio preference. It marks a recalibration of how central banks perceive safety, sovereignty, and macroeconomic risk.

The assumption that U.S. government bonds are the default “safe asset” is no longer taken for granted. Central banks—particularly those in non-Western economies—are signalling diminished confidence in U.S. macroeconomic stewardship and are repositioning accordingly.

Central banks are asking a simple but seismic question: What is truly safe? The emerging answer is gold.

When Trust Breaks Down, Gold Steps In

There are several forces driving this shift. The first is the erosion of trust in U.S. macroeconomic policy. The U.S. federal debt now exceeds US$35 trillion. Repeated debt ceiling standoffs have turned fiscal governance into political theatre. Inflation remains persistent, eroding real yields.

At the same time, the U.S. dollar has been weaponised through sanctions, asset freezes, and financial coercion. All these factors have made U.S. debt instruments less attractive to countries seeking autonomy and security in their reserve strategies.

Gold, by contrast, is neutral. It has no counterparty risk, cannot be frozen by foreign governments, and holds value across regimes and generations.

It is not just a hedge against inflation, but a hedge against dominance—especially for BRICS+ nations and others looking to reduce dependence on dollar-based systems.

In a multipolar world where geopolitical friction is rising and financial sovereignty is prized, gold is the ultimate “trust asset.” And the trend is accelerating.

Key Inflection Point: August 2025 – Gold surpasses U.S. Treasuries in share of foreign reserves

According to the World Gold Council, central banks added over 1,100 tonnes of gold to their reserves in the past 12 months alone—the highest annual net purchase since 1967.

This is not just about economic returns. It is about control, resilience, and strategic insulation. Foreign central banks are not abandoning U.S. Treasuries entirely—but they are recalibrating.

And that recalibration has symbolic weight: if even the world’s most liquid bond market can fall out of favour, no asset is immune to credibility risk.

Safe Assets Must Be Earned, Not Assumed

The broader lesson here is that macro policy credibility, transparency, predictability, and reputation are not optional—they are essential conditions for a country’s debt to be treated as “safe.”

Safe assets are not safe by decree. They must be earned through consistent discipline, clear rules, and responsible fiscal behaviour. When that trust erodes, markets react. Investor appetite shrinks, risk premiums rise, and governments face a dilemma: either restore credibility or pay more to borrow.

Even a superpower like the U.S. is now grappling with this reality. Long-term sustainability of public debt hinges not just on size, but on governance—whether investors believe the system is stable, prudent, and rules-based.

Fiscal consolidation is not just about reducing deficits—it’s about protecting reputation. Governments that lose that reputation cannot rely on history or size to save them. That is why clear fiscal anchors, institutional integrity, and predictable policy execution are now more important than ever.

Lessons for Malaysia and ASEAN

For smaller economies like Malaysia or Singapore, this is a crucial wake-up call. We cannot afford policy drift or fiscal complacency.

To maintain access to affordable capital, our credibility must remain intact. That means predictable macroeconomic frameworks, transparent debt management, and medium-term consolidation plans that are actually implemented—not just announced.

Malaysia, for example, needs to strengthen its fiscal governance through reforms under the Madani Economic Framework. Measures like targeted subsidies, tax base widening, and better public expenditure efficiency must be embedded within a rules-based system.

This ensures that our debt—whether in ringgit or foreign currency—continues to be seen as reliable by both domestic and international investors.

At the same time, reserve strategy must evolve. Bank Negara Malaysia and other regional central banks should review their asset composition to reflect new risks.

Diversification—including calibrated gold holdings—is no longer fringe thinking. It is prudent risk management in a world where “safe” no longer means what it used to.

Final Take: The True Safe Haven is Trust

This gold-versus-Treasuries crossover is not nostalgia—it is a wake-up call. The global monetary system is entering a new phase, where geopolitical alignments, fiscal discipline, and macro credibility all shape reserve choices.

Countries that fail to read this shift risk being left behind. In the end, neither gold nor Treasuries are intrinsically safe. The real reserve is trust. And trust must be earned—budget by budget, year by year, with no shortcuts. - DagangNews.com

Samirul Ariff Othman is an economist, international relations analyst, adjunct lecturer at Universiti Teknologi Petronas (UTP) and a senior consultant with Global Asia Consulting. The views expressed in this op-ed are entirely his own.

Layari kami terus di DagangNews.com

Orang ramai dipelawa menghantar artikel ke ruangan PARAFRASA di [email protected] mengikut ketetapan berikut:

1. Berbentuk analisis peribadi (Op-Ed) mengenai sesuatu isu atau topik, bukan plagiat

2. Topik yang mendapat perhatian segera dan utama ialah

a. berkaitan perniagaan, perdagangan, keusahawanan, pelaburan

b. Ekonomi MADANI

c. Pembangunan ekonomi negara dan negeri khusus

d. Sektor industri khusus seperti minyak sawit, getah, penerbangan, minyak dan gas

e. ESG

f. Hak pekerja, hak majikan, hak asasi manusia

3. Sains & Teknologi

a. Penemuan penyelidikan Sains & Teknologi serta teori dan konsep

b. Langkah mengkomersialkan produk berasaskan R&D

4. Kaedah penulisan

a) Sebaiknya seorang penulis sahaja pada penama.

b) Berbahasa Malaysia

c) Bahasa Inggeris diterima tetapi akan diterjemah ke Bahasa Malaysia

d) Editor akan memutuskan jika mahu mengekalkan Bahasa Inggeris

e) Tidak melebihi 1,000 patah perkataan dan tidak kurang daripada 600.

f) Jika disertakan gambar, juga amat digalakkan tetapi jangan guna Google (elak langgar hakcipta)

5. Hantar HANYA kepada DagangNews.com

a) Jika didapati artikel sama disiarkan di media lain kerana penulis menghantar merata-rata, nama penulis akan disenaraihitamkan.

b) Sila kemukakan Nama sebenar, Cadangan nama siaran dan emel untuk dihubungi (untuk rekod).